Sometimes we fall prey to an illusion of control in the midst of the frenzy. Saving and investing can feel intimidating. We don't want to lose money. Investing is much more fun when money is growing. Fear lies below the surface. What if the market falls. So we spend some time on google and discover asset allocation. Put some money in bonds and you'll be buffered against the inevitable fall of the market. You can adjust your bond allocation based on your age. You may even build in an extra allocation, called a bond tent, as you get closer to retirement.

The only problem - it doesn't work while you're building wealth.

It's particularly bad for proponents of financial independence who save up to some multiple of their living expenses. With "traditional" retirement, where you fix a retirement date, the closer you get to that date the more likely you are to want to protect the money you have saved. But what if that's turned on it's head a bit. If you just want to hit a savings target, you want the fastest way to get there. After you get to that number, then you may want to reallocate your account to protect the money you saved.

Others have done extensive work on how you withdraw money once you reach this target. This post is not attempting to add to that work. But using the same data, what can we say about saving for retirement?

Simple Case Study

What if you started saving for retirement at 25. You look at your annual expenses and you would like to be able to spend $40,000 per year. So you set a target of saving 25 times that amount or $1 million allowing you to be at the 4 percent rule. Of course, you increase the expenses and the amount each year to adjust for inflation, but to keep things simple we'll use numbers based on the purchasing power of a dollar in 2018. After budgeting you can save $2,000 per month toward this goal. How many months will it take you to reach $1 million?

That depends on what happens in the market, there is no way to know exactly how long it will take. But we can get a sense of how long it will take by looking at the historic returns in the market. To do this, we set a starting "year". E.g. picking 1987, had you deposited $2,000 in the starting in May of 1987, it would have been worth $2,006.95 the next month giving you a total of $4,006.95 after adding the next $2000. The following month the market had gone down the $4006 would have decreased in value to $3704 giving a total of $5704 after again adding the next $2000. If you had instead started investing in 1984, by the third month you would have been at a total of $6235. If we do this for every different starting year in recorded history we start to get a picture of what range of returns you would expect from the stock market.

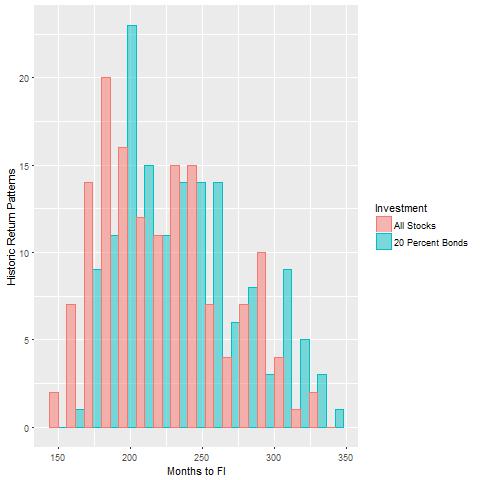

If you started investing in 1987, it would have taken 243 months or just over 20 years to get to $1 million. If you started in 1984, it would have taken you 230 months. If we look at starting in all the historic years from 1871 all the way to starting in 2017* there are 147 different historic return patterns that help us estimate how much time it will take to reach $1 million. On average, it would take you 224 months or just shy of 19 years. But if you are fortunate, there are a couple of patterns that would have you retiring in 13 years. To get a sense of all the various patterns, look at the following histogram.

You could be throwing your retirement part anywhere from 13 years to 28 years from now. Still, it's better than putting cash in a savings account that just keeps up with inflation, which would have you retiring 42 years down the road. If you hit a market downturn, your timeline for retirement stretches out. So perhaps you could protect your money by allocating some to bonds. Then your returns will be "smoother" according to the prevailing theory. So if you don't lose as much money, perhaps you would get to your retirement faster when the market goes back up... So take a look at what happens if you allocate 20 percent of your retirement to bonds.

Turns out that you just added a year to your expected retirement date. In the best case scenario, you were able to retire 4 months sooner because of your bond allocation. In the worst case scenario, you extended your retirement date by 10 years. If you use the 100 minus your current age bond allocation it is even worse.

Your expected retirement date gets pushed back another year. That is, if you just invested in the market you would have expected to reached your goal 2 years earlier. Is your bond allocation worth working another 2 years?

Conclusion

I have run studies at different savings rates and seen this pattern in every one I have looked at thus far. The impact on retirement date is asymmetric in every case. The few times that a bond allocation helps you out, it provides very little help. You may retire a few months early. But when it hurts you, the pain can be extreme. If you are edging toward a retirement date that isn't optional, then it may make sense to defend against a downturn using bonds. But if you have the flexibility to be saving toward a goal, and only when you hit that goal will you retire, then your bond allocation isn't helping you.

So why is that? My theory is that you're not going to hit your savings goal in a downturn. It doesn't matter that you dip low. You're going to reach your goal when the market is on an upturn. And that's when the bond allocation is hurting the portfolio performance.

Turns out this post created some controversy. To follow-up on that controversy, take a look at a case study about bond allocation formulated as a letter to reddit, because why not?

* - When you start in 2017 and reach the end of the year, for this simulation the next year starts over at 1871. This ensures that each year in the record is sampled the same number of times.

Wikimedia Photo Credit